ATTENTION: PARENTS OVER THE AGE OF 35

Have A Family & Need A Predictable Prosperity Plan?

Let Us Show You How To Build A Multi-Million Dollar Legacy for Yourself, Your Spouse & Your Kids... Faster and Easier Than You Ever Thought Possible. You Don't Need To Be a Millionaire or Even Close To It To Start Using This Strategy Today.

Click The Video To Learn How

As Seen On...

Who’s Behind WealthyIQ?

Jeff & Tina Ziegler

Jeff & Tina Ziegler became financially free in 2006 because their passive income had exceeded their turn-key expense. However, in 2016 they almost lost everything. As a result, they learned to build a stronger foundation using easy to understand financial strategies that are far superior and less risky than what’s commonly taught in personal finance methods. Jeff & Tina’s on-demand masterclass shows attendees how to plug leaks, creating more cash flow so they can reach financial independence in 5-10 years instead of 30.

They show attendees how to boost their financial IQ and achieve financial security by replacing their income with smart wealth-building strategies. This unique method focuses on resetting and realigning your financial mindset, habits, and goals to optimize your wealth-building efforts. Regardless of age, income, social status, investment knowledge, or experience — you can live a life of impact with Jeff & Tina’s Lifetime Wealth Acceleration System.

Our Boys: Dalton, Garrett, Cade, Chase & Jett

We are a mission-driven family, and all five of our boys use our Lifetime Wealth Acceleration System. We know you have a dream for your family, and we created this masterclass to learn from our mistakes and to make sure you achieve yours. Think of how much better your future would be if you owned your Cash Flow and had more accumulated assets that produce a passive income in record time. Imagine how much more generous you could be to others when you don’t have a single financial worry in the world.

Our Boys: Dalton, Garrett, Cade, Chase & Jett

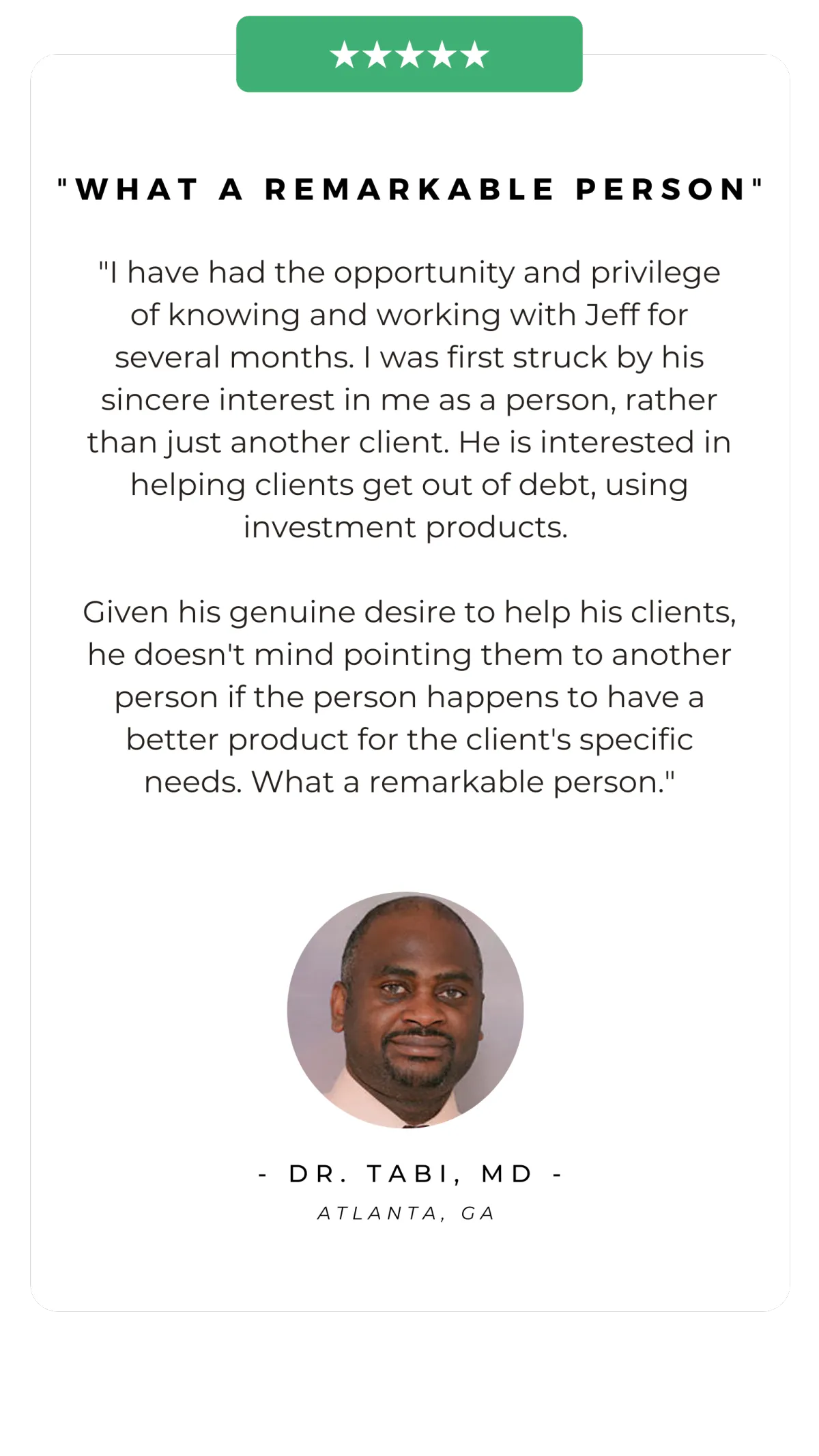

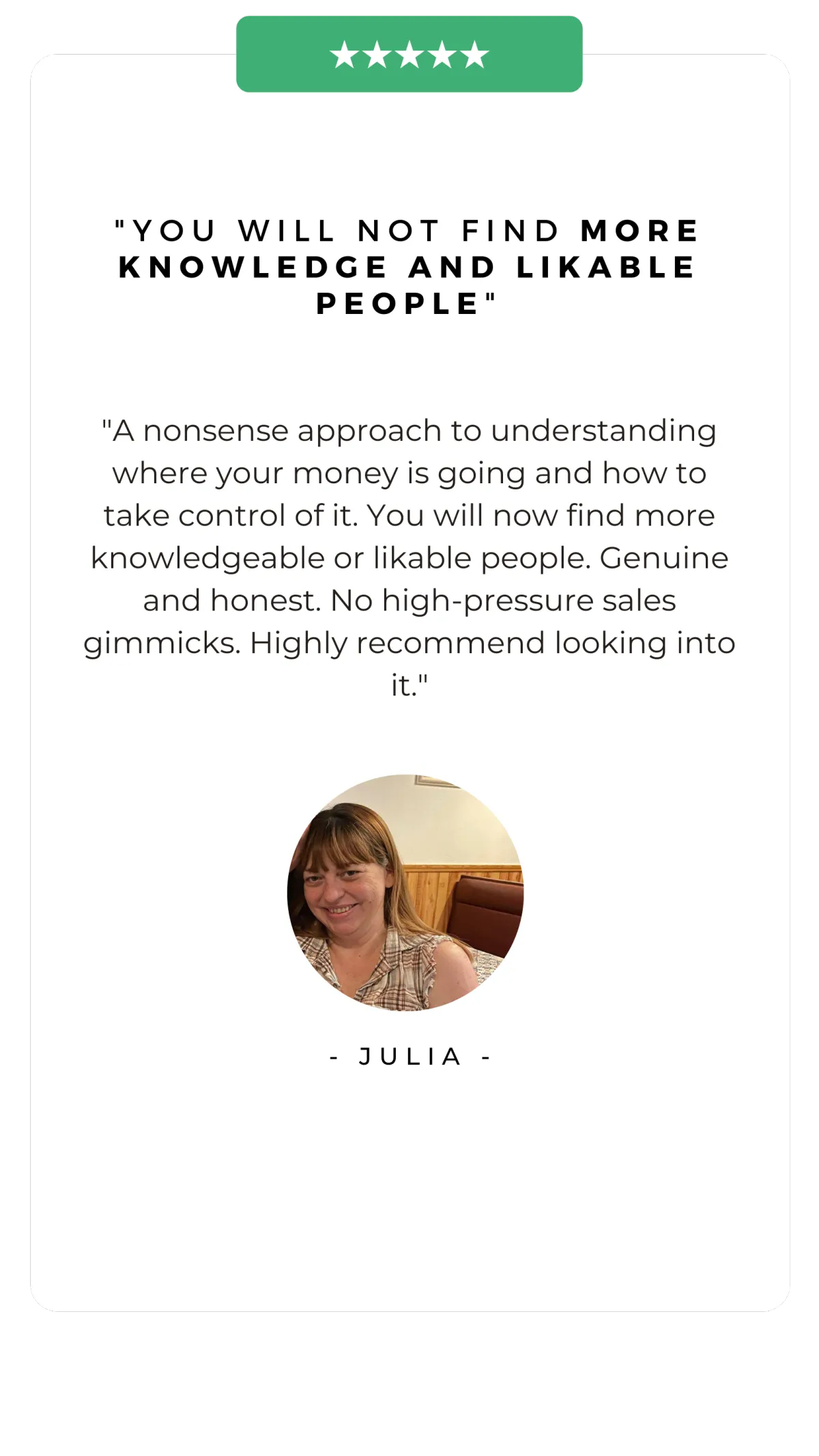

Don’t Just Take Our Word For It…

See what others have said about their experience:

12265 Oracle Blvd Suite #115,

12265 Oracle Blvd Suite #115,

Colorado Springs, CO 80921

Colorado Springs, CO 80921

© 2024 WealthyIQ, LLC - All Rights Reserved

© 2024 WealthyIQ, LLC - All Rights Reserved